Well, featuring fire and flood at least.

As we’ve noted before, the ‘1996 exemption‘ to the bedroom tax only applied if one was in the same property or if:

the dwelling so occupied was not the same by reason only that the change was caused by a fire, flood, explosion or natural catastrophe rendering the dwelling occupied as the home on the first date uninhabitable;

My recorded view is that this is strict (‘by reason only’) and not a general force majeure clause that would extend to decants for demolition or such-like.

A Liverpool FTT adopted a fairly open approach to this. (The decision notice is here and on the FTT decisions page.)

{kind=link}

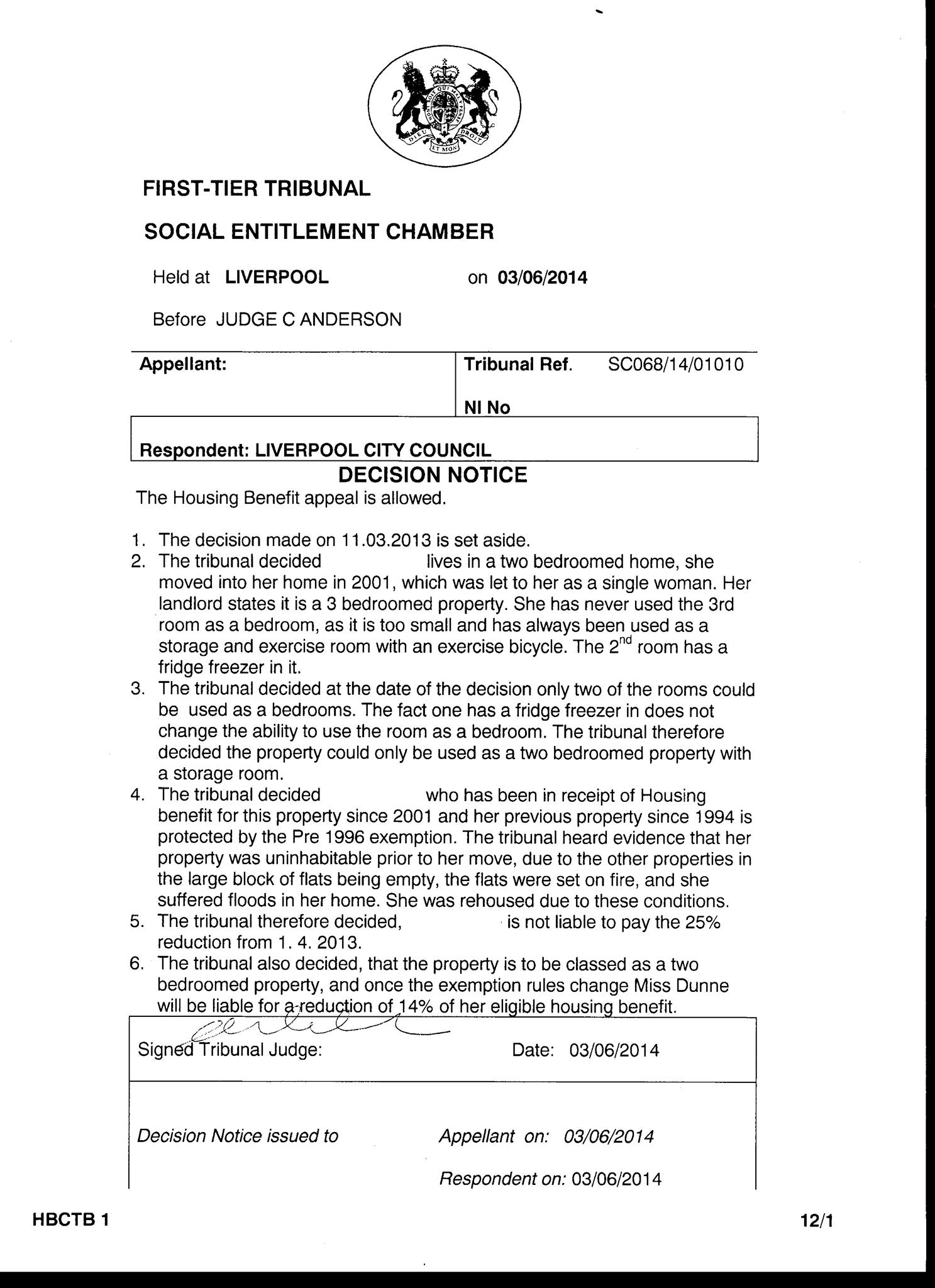

The unnamed appellant had been moved from her previous property in 2001.

The tribunal heard evidence that her property was uninhabitable prior to her move, due to the other properties in the large block of flats being empty, the flats were set on fire, and she suffered floods in her home. She was rehoused due to these conditions.

The other flats being empty is the clue – there was surely a block decant for demolition or redevelopment going on. But the appellant’s accepted evidence of there having been both fire and flood (one would have done!) at the property was taken as the reason for her rehousing. And of course it could well be so, an urgent move that took place before a planned decant move.

Unlikely to be the most common of situations, but on the accepted evidence, a perfectly proper application of the 1996 exemption.

It is also worth noting that a supplemental argument that a room in the current property was not a bedroom on the basis of room use failed, because, although the room had a fridge freezer in it and was not used as a bedroom, that ‘does not change the ability to use the room as a bedroom’.

(At least one of us on NL is a Wagner fan. But it isn’t me. It is important to make this clear.)

Giles- this homes was a previously classified as a three bedroomed home, not only was the appeal allowed/ won on the Pre-1996 issue (demolition) fire/flood, (we believe the first in the country, correct us if we are wrong!). But also the smallest 3rd room upstairs was also exempted as the room has never been used as a bedroom and is under 70 square feet!!! So after the Pre 1996 exemption ends on the 02/03/14 the bedroom tax will be further reduced from 25% to 14% what a victory for this tenant in Kirkdale, Liverpool!!! We will let you have the SOR as soon as we get it!!!

Juliet – yes, I saw that was a further one room exempted on the now usual size grounds.

I believe this is the first contested 1996 exemption case, certainly I haven’t heard of any others.

I had a similar case where client had been decanted…HB department of Council gave in without a tribunal and gave him indefinite DHP….notes in CPAG legislation book suggest that a decant or similar, or at least a move beyond the tenant’s control should be included as an exemption.

Chris – no the 1996 exemption where there has been a move is not a general ‘decant’ or force majeure exemption. Note that the FTT in this case was careful to conclude the tenant had been moved because of fire and flood.

Indefinite DHP is a good result, but is not ‘giving in’ – it is upholding the HB decision.

In this case it was giving in…citing the notes in the above book was enough to stand them down as I was asking for an appeal…I couldn’t justify to client continuing on appeal because of the DHP and the regulation-tightening by 31st March